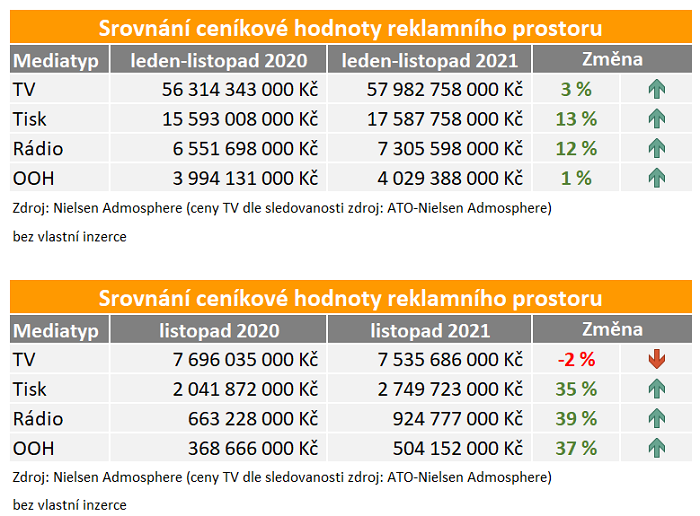

In this year’s eleven months, all media types show higher volumes of ad investments than in the comparable period last year.

This November, the monitored volume of ad investments in the media remains above the level of the same month last year. As the AdIntel data provided by Nielsen Admosphere shows, investments in print, radio and OOH increased by nearly 40% in the eleventh month of this year, which does not apply to TV.

The monitored volume of TV investments was two percent lower. However, TV receives nearly two thirds of ad investments out of all media available for comparison.

In the period from January to November 2021, the monitored volume of media ad investments is higher by more than 5%. All media types report better results than in the comparable period last year.

Source: Nielsen Admosphere (TV costs by viewership, source: ATO-Nielsen Admosphere) Without own advertising

The media overview by monitored investments excludes the internet as the monitoring only covers display advertising, thus omitting other online ad formats.

We reiterate that the volumes monitored do not correspond to the actual investments; they are prepared based on list prices.

Source: mediaguru.cz